STRATEGY IN ACTION: MEET JOHN

John earns $1,000,000 in 1099 income from his business in 2025 and faces a $400,000 tax obligation (estimated 40% federal/state tax rate).

To reduce his taxes, John purchases 29 solar carports at $35,000 each, for an approximate cost of $1,000,000. He contributes $600,000 (60%) as his initial investment, with the remaining 40% financed through a third-party loan.

Under Section 179, his depreciable basis is 75% of his purchase price, resulting in $750,000 in depreciation, resulting in an adjusted taxable income of $250,000.

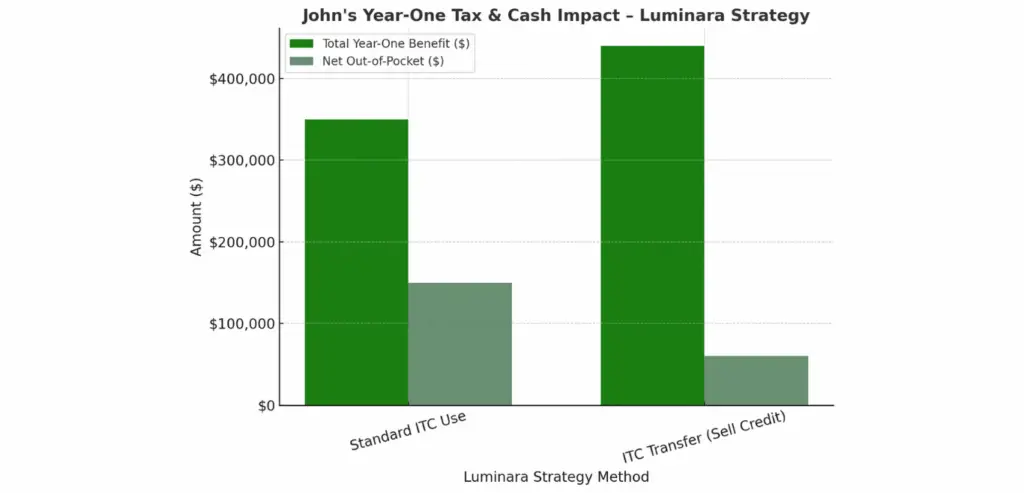

John qualifies for a 50% Investment Tax Credit (ITC) of $500,000. He keeps the tax credit which offsets his $600,000 purchase n the solar carports, reducing his out-of-pocket cost to $100,000.

John’s upfront cost ($600,000) is significantly offset by the Investment Tax Credit ($500,000) and tax savings from accelerated depreciation ($300,000). After applying these incentives, not only does he cover his initial cash payment, but he walks away with $200,000 in net cash — all while reducing his taxable income and positioning himself for future returns on the solar project.